Welcome to the November edition of the AFGC’s Economic Bulletin: our quarterly round up of the latest economic news impacting our industry, including consumer prices, input costs, exchange rates and commodity prices.

In this edition we also take a look at international shipping, energy, labour and consumer sentiment.

Analysis

The recent quarterly data highlights a complex economic landscape that will undoubtedly impact the fast-moving consumer goods (FMCG) sector in the coming months. While the last quarter witnessed growth in the value of food retail sales, this uptick was primarily driven by shelf price increases. Given that consumers are facing heightened cost-of-living pressures across the board, they are likely to respond by changing consumption patterns and trading down.

On the input cost front, the data indicates that some of the pressure in food input prices has started to recede as overall international food commodity prices have declined since their peak in March 2022. This shift is reflected domestically in a decrease of the input producer price index for food product manufacturing. However, the nuanced cost landscape reveals persistent pressure on certain inputs, both on the global and domestic front. Suppliers must balance the benefits of cost reductions with the challenges posed by changing commodity markets.

Currency fluctuations, illustrated by the depreciation of the Australian dollar against major currencies, add an additional layer of costs for businesses reliant on imported ingredients, packaging materials and finished goods. As international shipping costs stabilise, businesses will have to take a strategic approach for mitigating the impact of these currency fluctuations on import and export dynamics, ensuring competitive pricing and supply chain resilience.

Fluctuations in energy costs and a robust, yet cautious, labour market underscore the need for companies to optimise operational efficiency and workforce management. In response to the rising prices of natural gas and increasing expectations for less carbon-intensive manufacturing practices, businesses are encouraged to re-assess their energy consumption strategies.

Looking ahead, the forecast for the sector hinges on its ability to adapt to these dynamic economic variables. Strategic pricing, supply chain resilience, and consumer-centric innovation will be crucial for companies to thrive in an environment marked by inflation, currency volatility, and a grim consumer sentiment.

1. Consumer prices

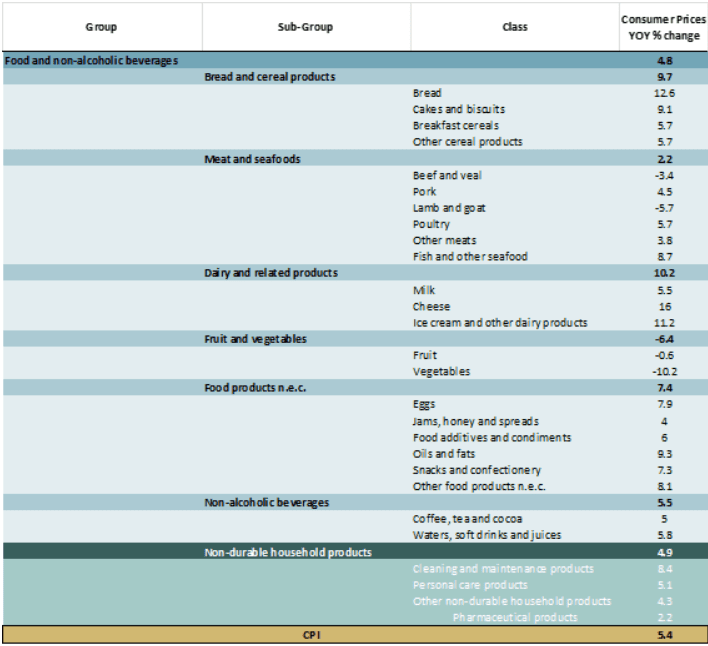

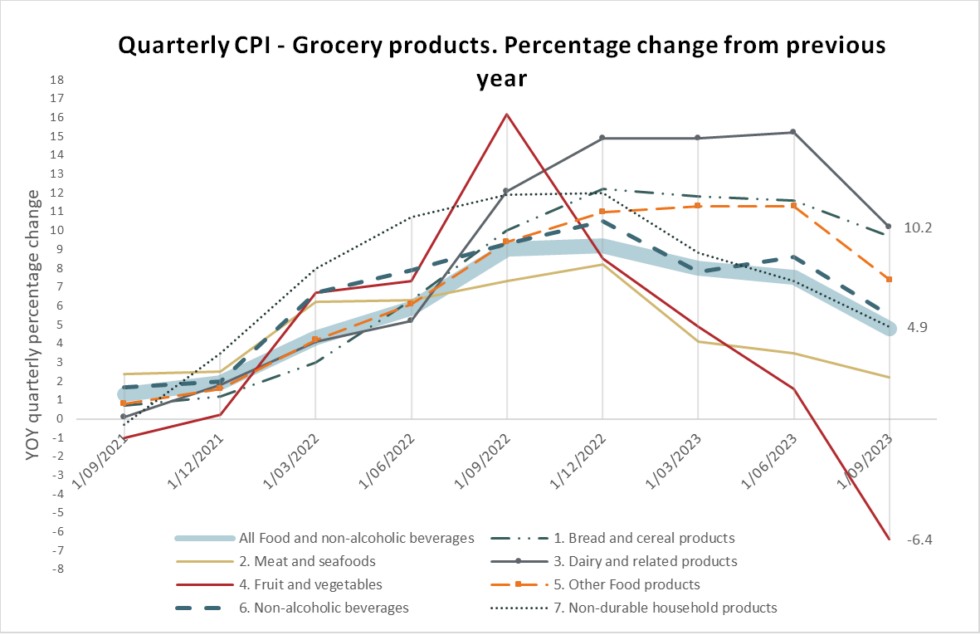

According to the Australian Bureau of Statistics (ABS) Consumer Price Index data, food and non-alcoholic beverages prices registered a 4.8% year on year increase in September 2023.

While this quarter presented a stabilisation in the rate of inflation for most product categories in the FMCG sector, with some subcategories even having a YOY price decreases, inflation remains high.

Key YoY price changes were:

Vegetables -10.2%

Lamb & Goat -5.7%

Beef & Veal -3.4%

Oils & fats 9.3%

Ice cream and other dairy 11.2%

Bread 12.6%

Overall, year on year inflation was 5.4% in September 2023.

Source: ABS. Producer Price Indexes. Nov 2023.

Source: ABS. Consumer Price Index. November 2023.

2. Input costs

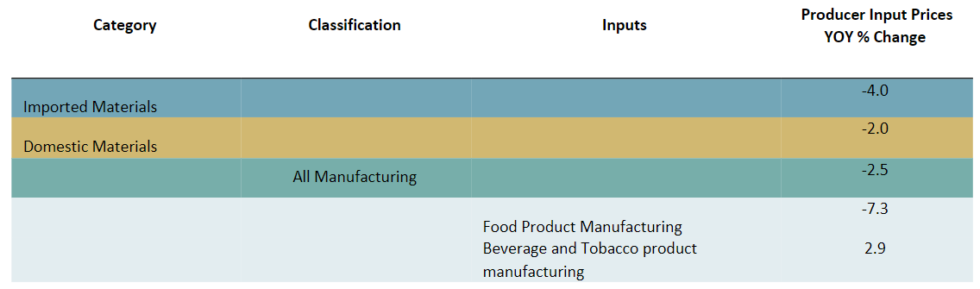

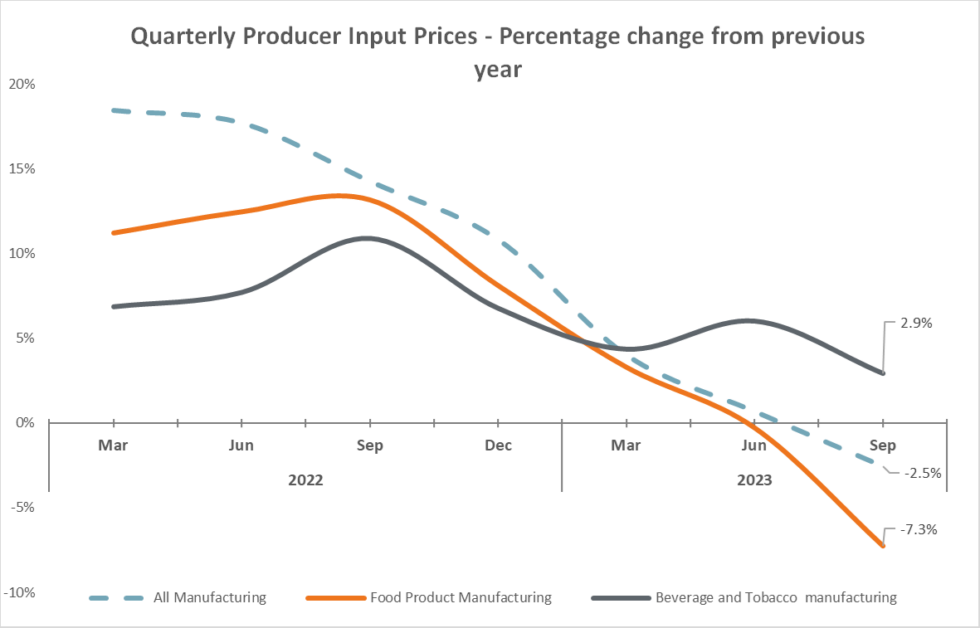

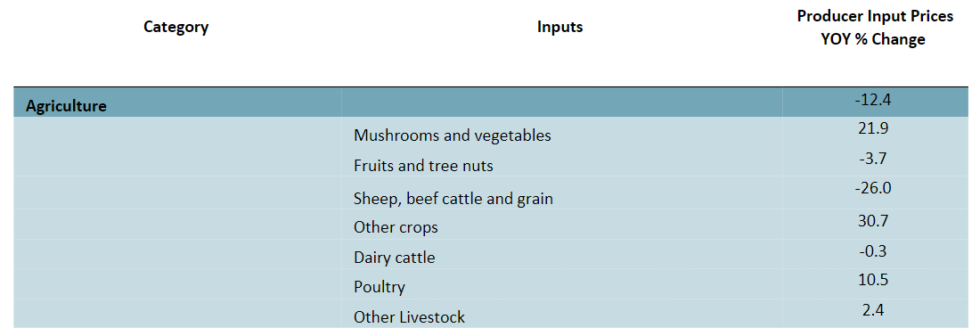

According to data from the ABS’ Producer Prices Indexes, food product input prices recorded a year-on-year decrease of 7.3% in September 2023.

Beverage and Tobacco inputs increased 2.9% in the same period.

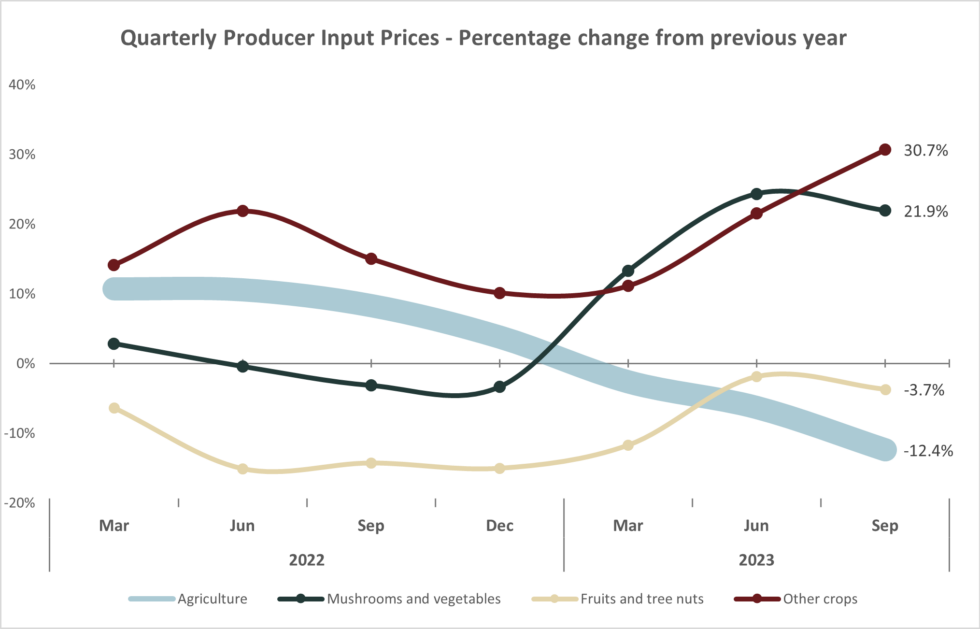

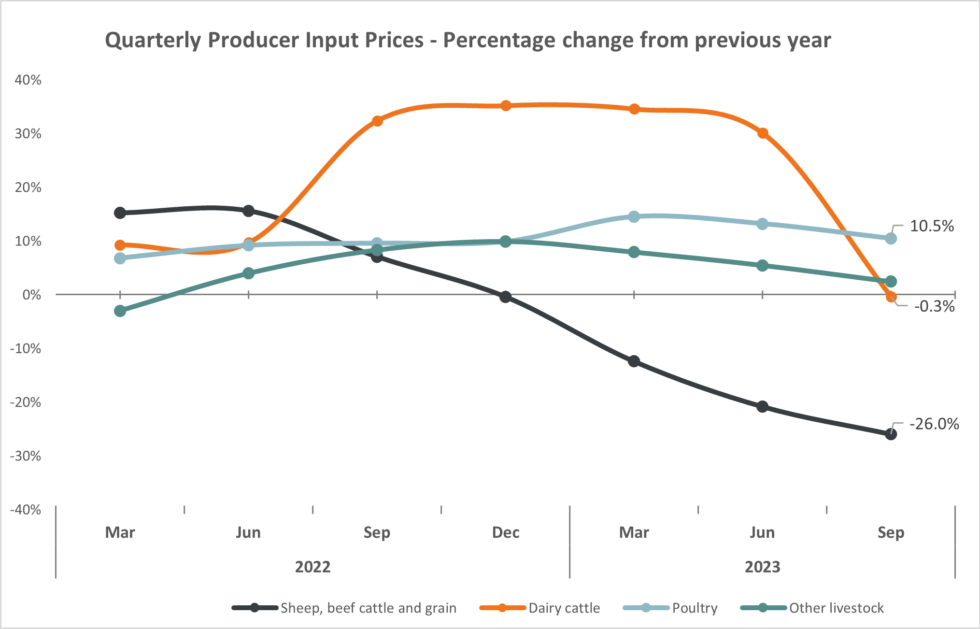

Agricultural inputs recorded a year-on-year decrease of 12.4% in the same period, driven by a large decrease in meat prices, however not all agricultural inputs saw price reductions.

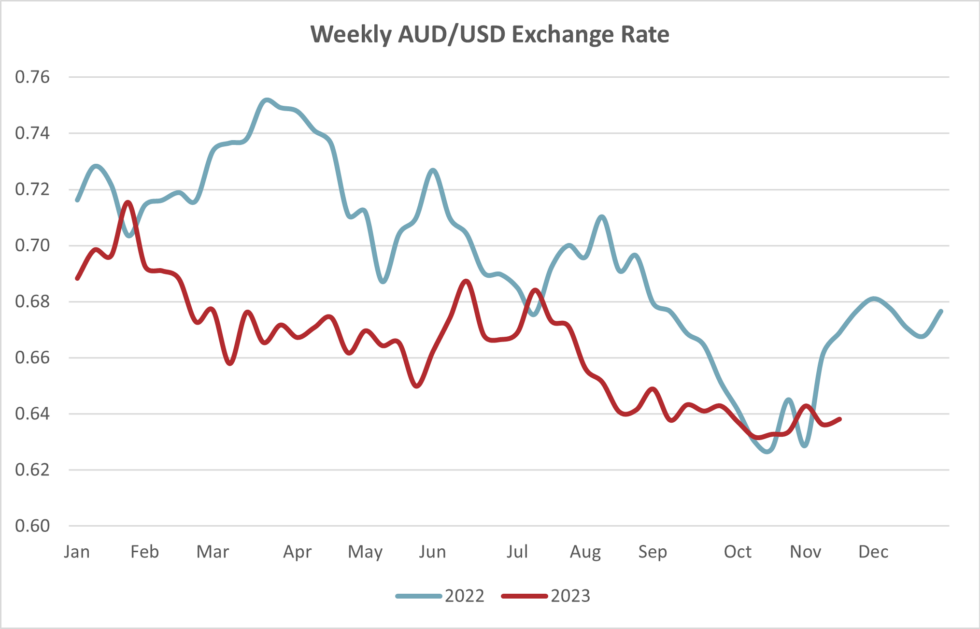

In November 2023 the AUD/USD monthly average exchange rate has fluctuated around the 0.64 mark, representing a 0.5% year on year depreciation.

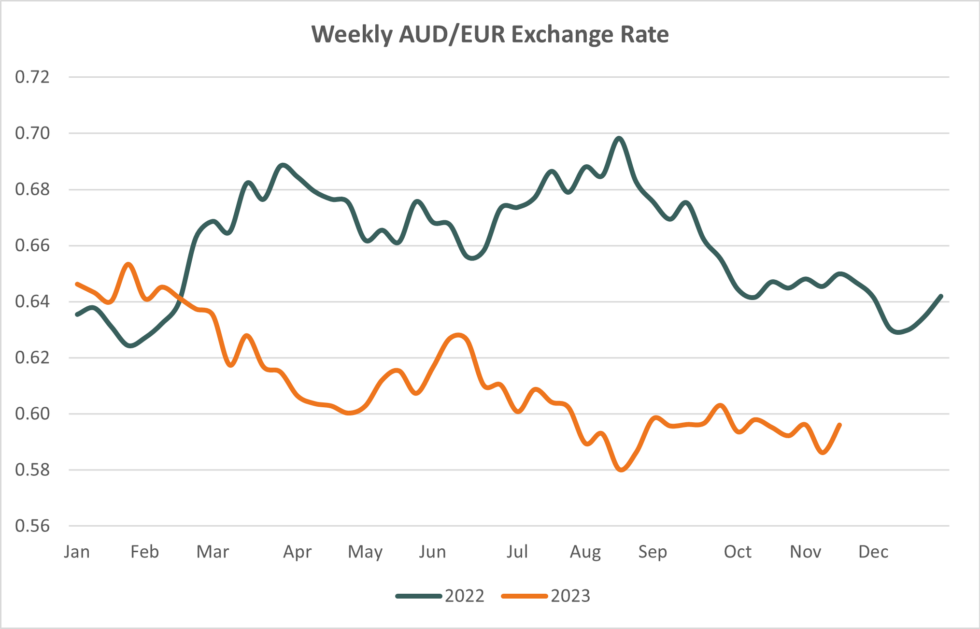

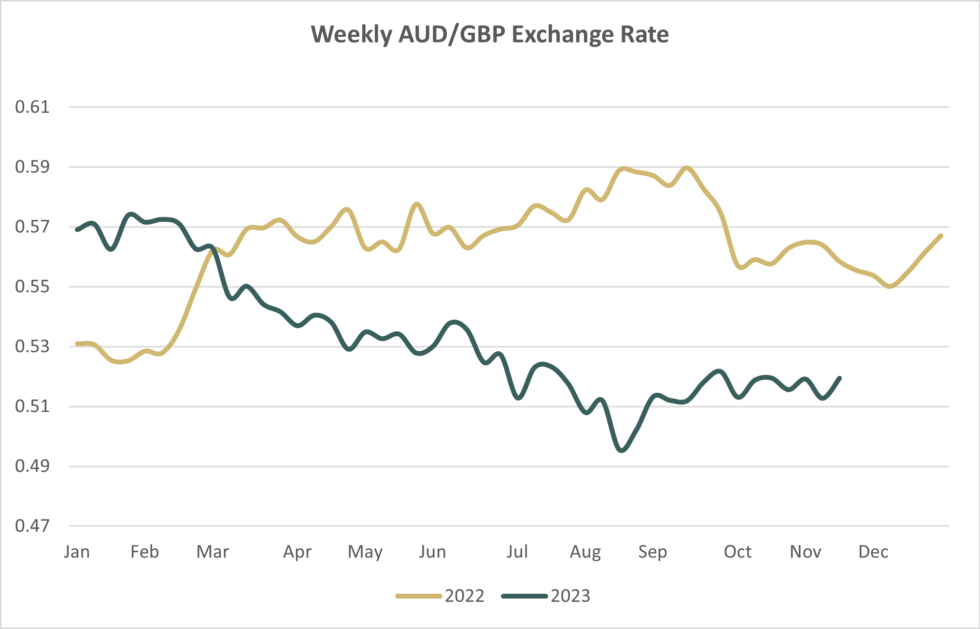

The AUD/EUR and AUD/GBP monthly average exchange rates have decreased 8.18% and 7.91% respectively in the same period.

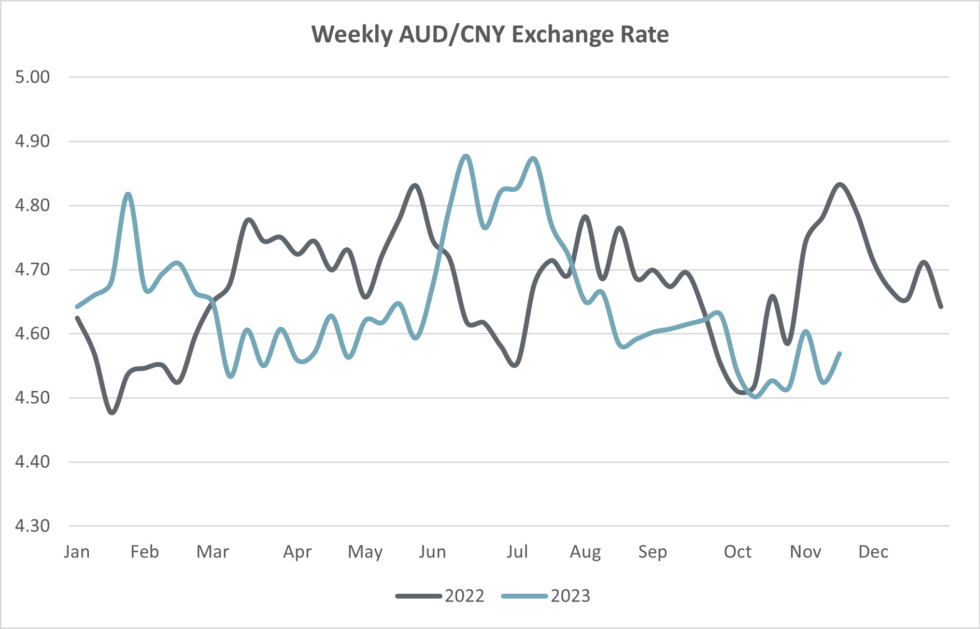

The monthly average AUD/CNY exchange rate in November 2023 is 1.58% below the value in the previous year.

Source: Yahoo Finance.

Source: Yahoo Finance.

Source: Yahoo Finance.

Source: Yahoo Finance.

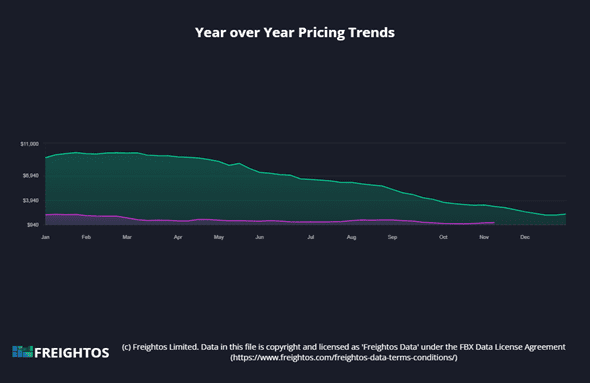

4. International shipping

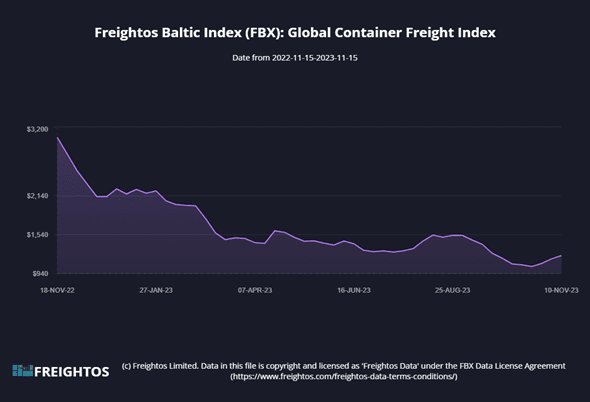

In the last month International Ocean Freight Shipping prices have slightly increased, most likely due to increased seasonal demand. However, international ocean shipping prices have stabilised at pre-covid levels for main international routes.

The Freightos Baltic Global Container index (FBX) suggests a significant year-on-year decrease of 69% in global shipping prices in November 2023.

Anecdotal information suggests domestic ocean freight costs remain above the global average.

Source: Freightos. Freightos Baltic Index (FBX) Global Container Index. November 2023

Source: Freightos. Freightos Baltic Index (FBX) Global Container Index. November 2023

5. Commodities

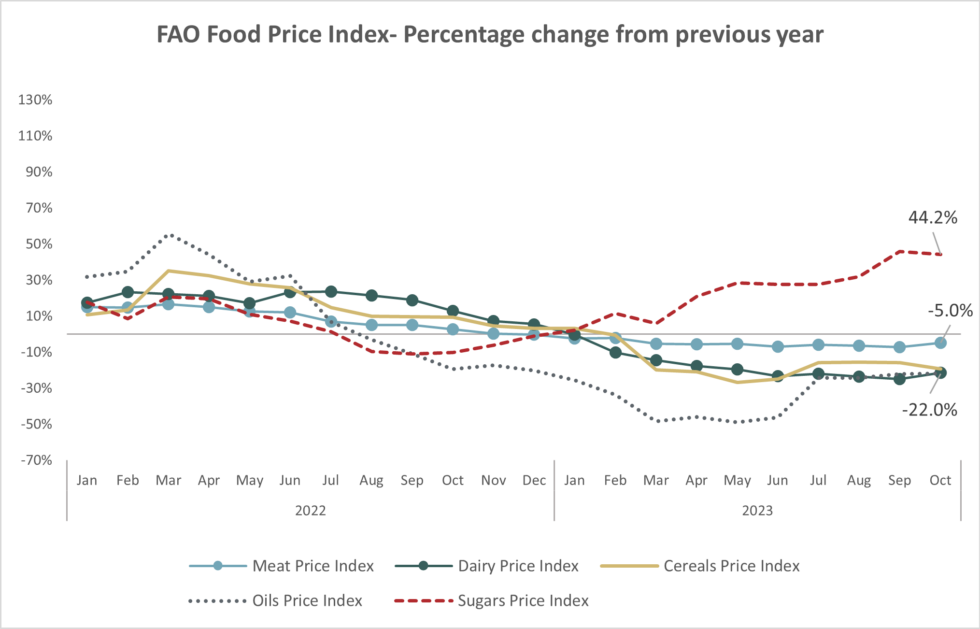

The following information is based on monthly global data from the Food and Agriculture Organisation (FAO) of the United Nations. The FAO Food Price Index (FFPI) is a trade-weighted average of the prices of food commodities spanning the key agricultural markets for cereals, vegetable oils, sugar, meat and dairy products.

FAO’s Monthly Food Price Index (FFPI) declined in October 2023, continuing the downward trend of the last few months, driven by drops in monthly prices of meat, cereal, vegetable oil and dairy products. According to FAO’s index, international prices of food commodities have decreased 12.5% since October 2022, despite a 44.2% year-on-year increase in sugar prices.

FAO’s Dairy Monthly Price Index has decreased 21.4% since October 2022. In October, international cheese prices slightly decreased due to the ongoing depreciation of the Euro against the US Dollar and a rise in export capacity in Oceania. However, global milk powder prices experienced a significant rise, mainly attributed to heightened import demand for short- and long-term supplies, particularly from Northeast Asia. The increase was further fuelled by limited milk availability in Western Europe and uncertainty regarding the impact of El Niño on upcoming milk production in Oceania.

FAO’s Cereal Price Index has decreased 19.3% since October 2022. In October, global wheat prices experienced a 1.9 percent decline, attributed to an abundance of supply from the USA and robust competition among exporters. Although diminished maize supplies in Argentina contributed to upward pressure on global maize prices, this effect was mitigated by a high yield in the USA and intense competition from Brazil.

FAO’s Vegetable Oil Price Index has decrease 22% since October 2022. International palm oil prices continued to drop in October due to seasonally higher outputs in leading producing countries as well as subdued import demand. The drop in international palm oil prices more than offset the higher price of soy, sunflower, and rapeseed oil.

FAO’s Sugar Price Index has increased 44.2% since October 2022. Despite a slight dip in international sugar prices in the past month, prices remain high when compared to the previous year. The decrease observed in October 2023 can be attributed to robust sugar production in Brazil, coupled with the depreciation of the Brazilian real against the US Dollar and reduced ethanol prices in Brazil. However, these downward pressures were somewhat offset by ongoing concerns about a constrained global supply outlook in the 2023/24 season, as well as shipment delays from Brazil.

Source: FAO. Monthly Real Food Price Indices. November 2023

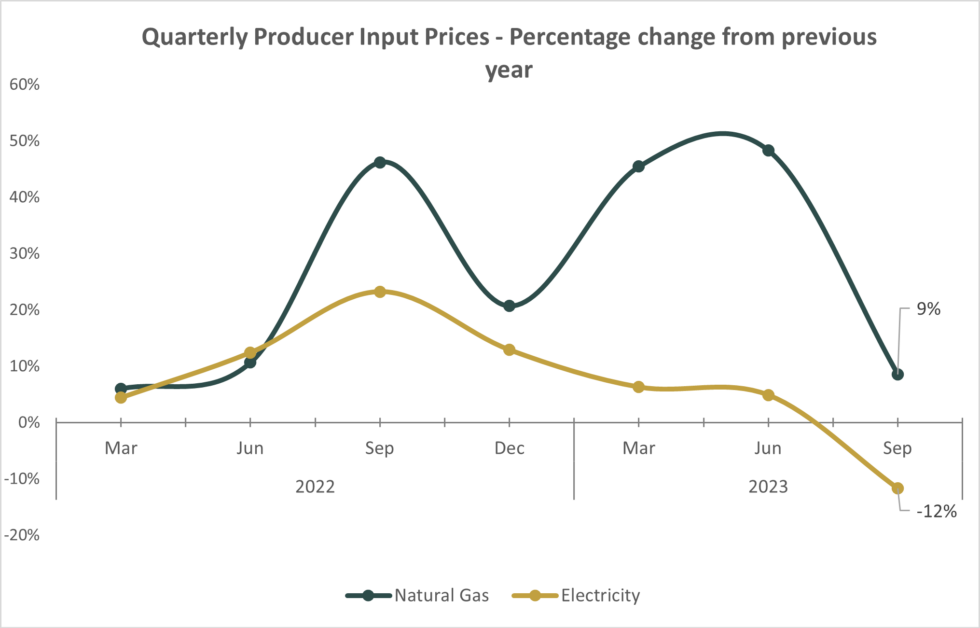

6. Energy

According to ABS producer price data, natural gas input prices increased by 8.5% in September 2023 compared to September 2022.

Electricity input prices decreased 11.7% in the same period.

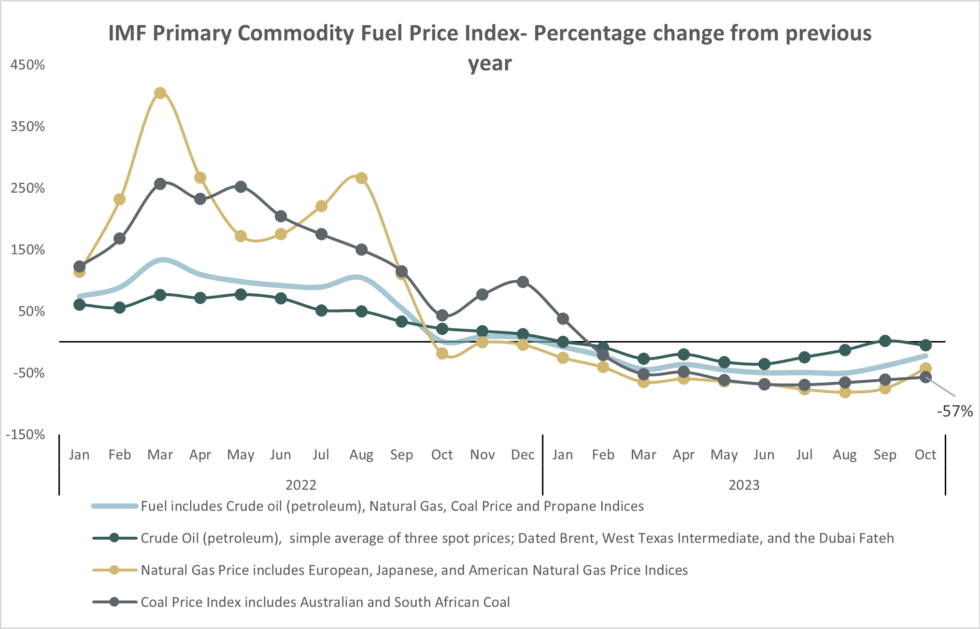

According to the International Monetary Fund’s (IMF) Primary Commodity Fuel Price Index, global fuel prices in October 2023 were 22% below their level in October 2022.

International crude oil, natural gas and coal prices presented YoY decreases of 6%, 43% and 57% respectively compared to October 2022.

Source: ABS. Producer Price Indexes. November 2023.

Source: IMF. Primary Commodity Prices. November 2023

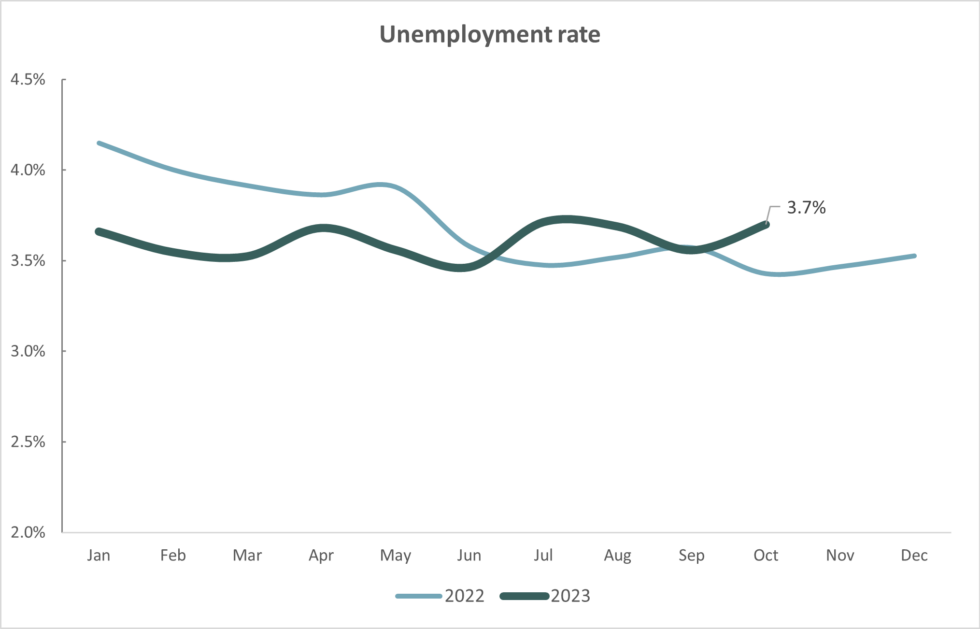

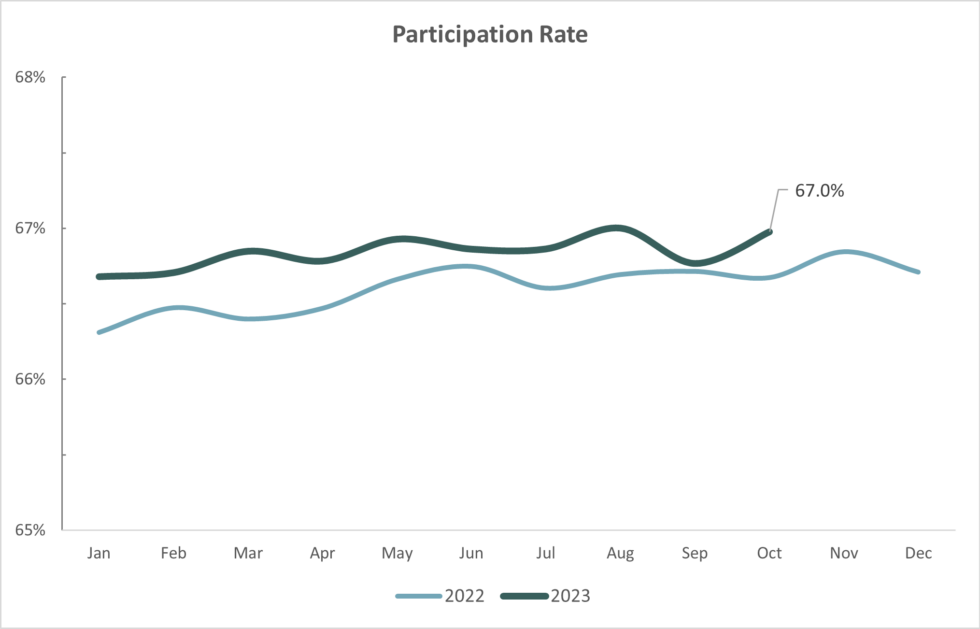

7. Labour

The Australian labour market remains strong and tight.

According to ABS’ Labour Force Statistics in October 2023 the unemployment rate has remained stable, around the 3.7% mark since January 2023.

Participation rate has remained stable around the 66.8% mark since November 2022.

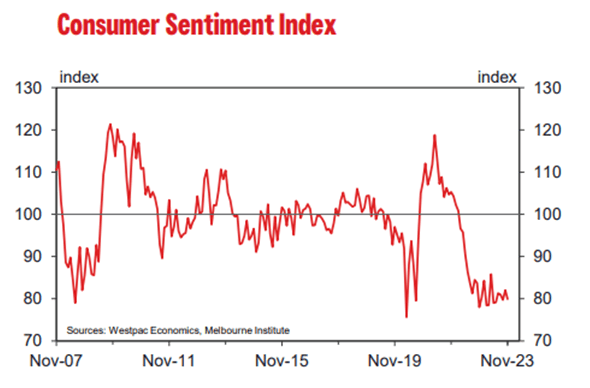

Although unemployment has remained steady at historical low levels, Westpac’s Consumer Sentiment Index suggests consumers expect unemployment to rise in the year ahead.

Source: ABS. Labour Force Australia. November 2023.

Source: ABS. Labour Force Australia. November 2023.

Source: ABS. Labour Force Australia. November 2023.

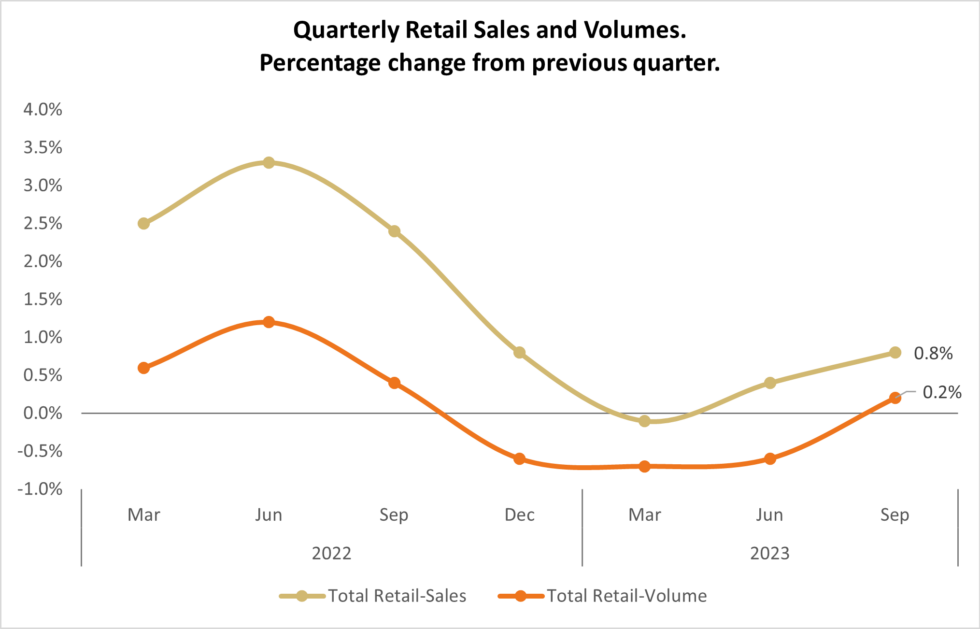

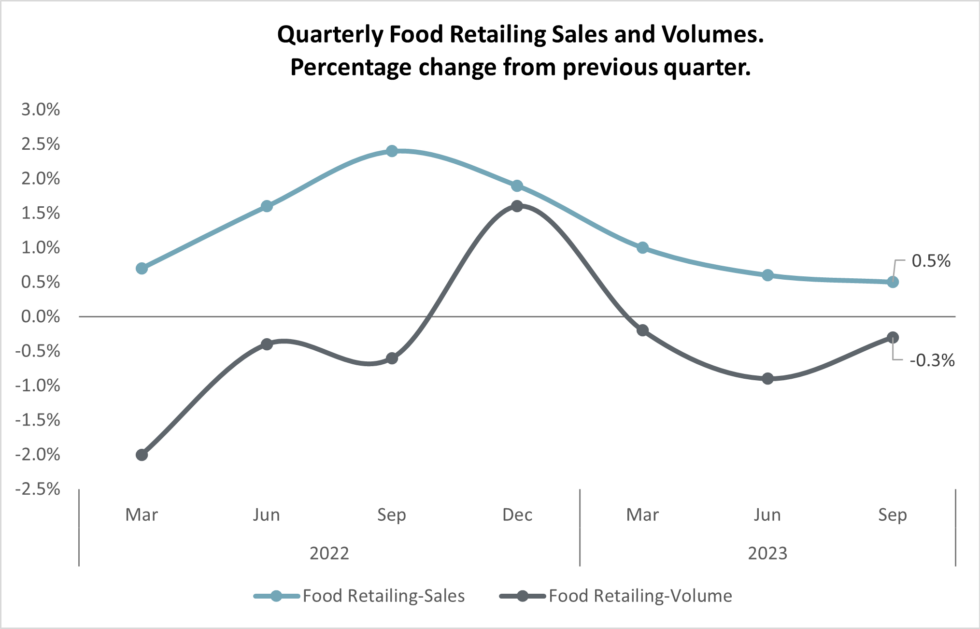

8. Retail sales

The Australian retail sales increased 0.8% in September 2023 from the previous quarter. However, when measured in volume terms, sales increased by 0.2% in the same period.

While total retail sales went up from last quarter, this increase has been driven by elevated price inflation. There has been a significant slowdown in non-food retail sales in the last two quarters.

Australian supermarket sales rose 0.5% in September from the previous quarter, primarily driven by price increases.

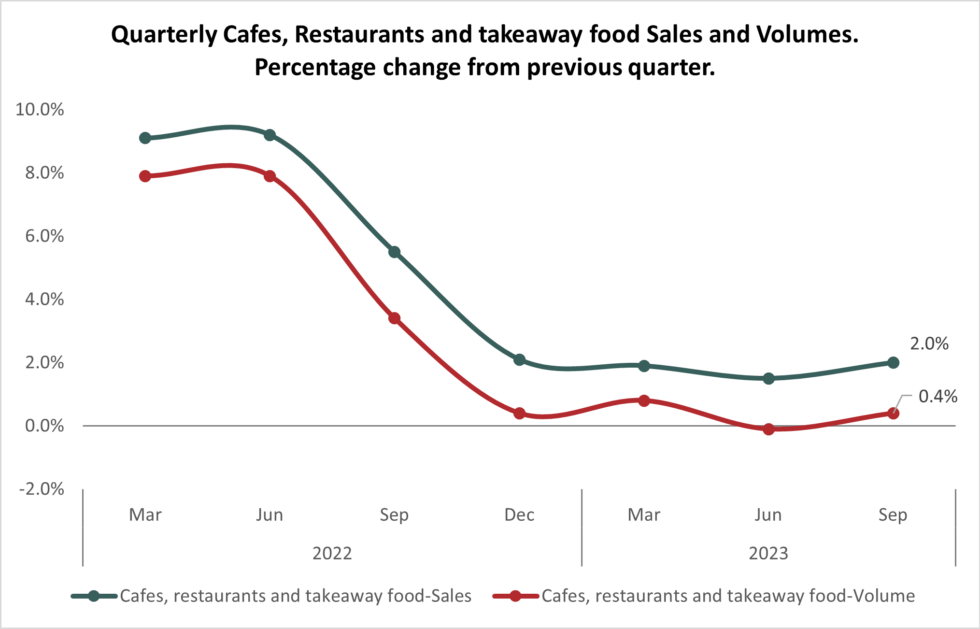

Café, restaurant, and takeaway sales increased 2% in the quarter.

Source: ABS. Retail Trade Australia. November 2023.

Source: ABS. Retail Trade Australia. November 2023.

Source: ABS. Retail Trade Australia. November 2023.

9. Consumer confidence

The Westpac-Melbourne Institute Consumer Sentiment Index declined 2.6% from October to November as a result of the latest Reserve Bank’s rate rise, which has reignited concerns about cost-of-living pressures and the prospect of further rate rises.

The Index has returned to the deeply pessimistic levels that had prevailed since the middle of last year. This pessimism will have an impact on spending attitudes in the lead up to Christmas as 40% of the respondents advised they plan to “spend less on gifts than last year”.

Source: Westpac Economics, Melbourne Institute. Consumer Sentiment Report. November 2023.

The figures presented are current at the time of publication and are subject to updates and revisions.